What is an offshore company?

Cryptocurrencies & Offshore company

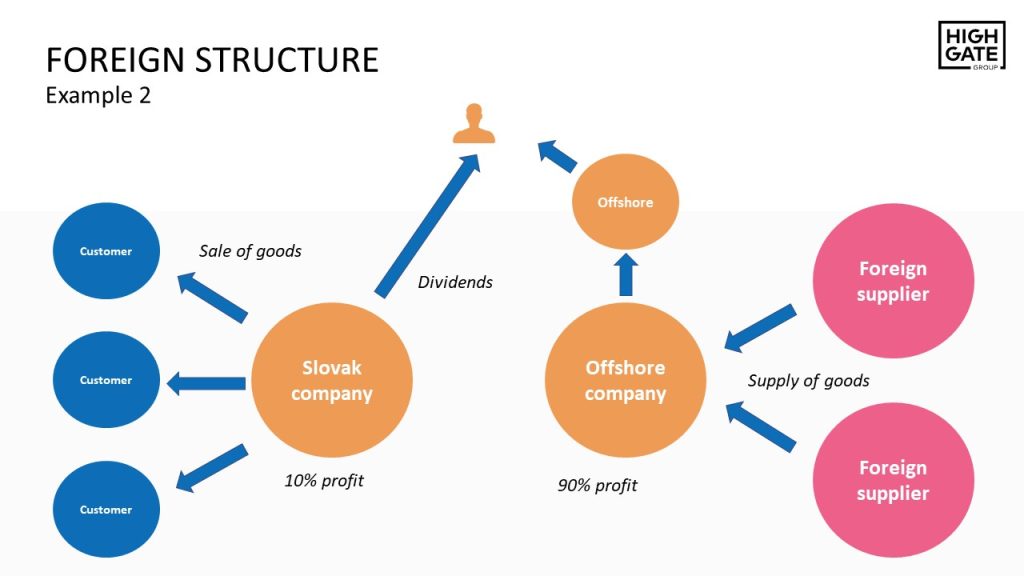

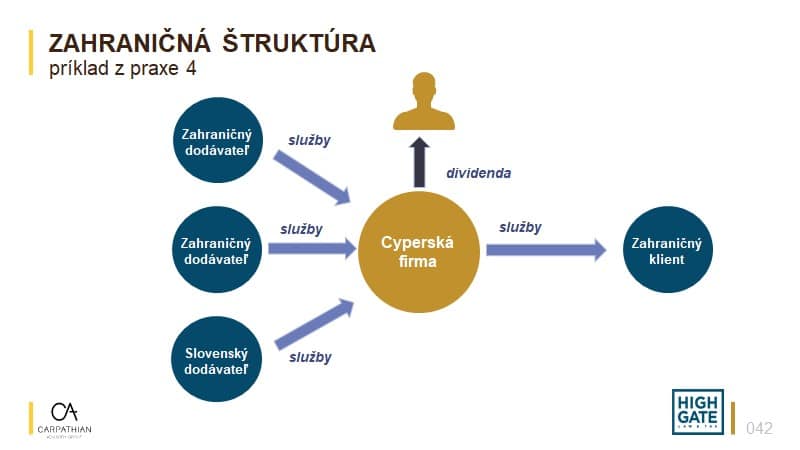

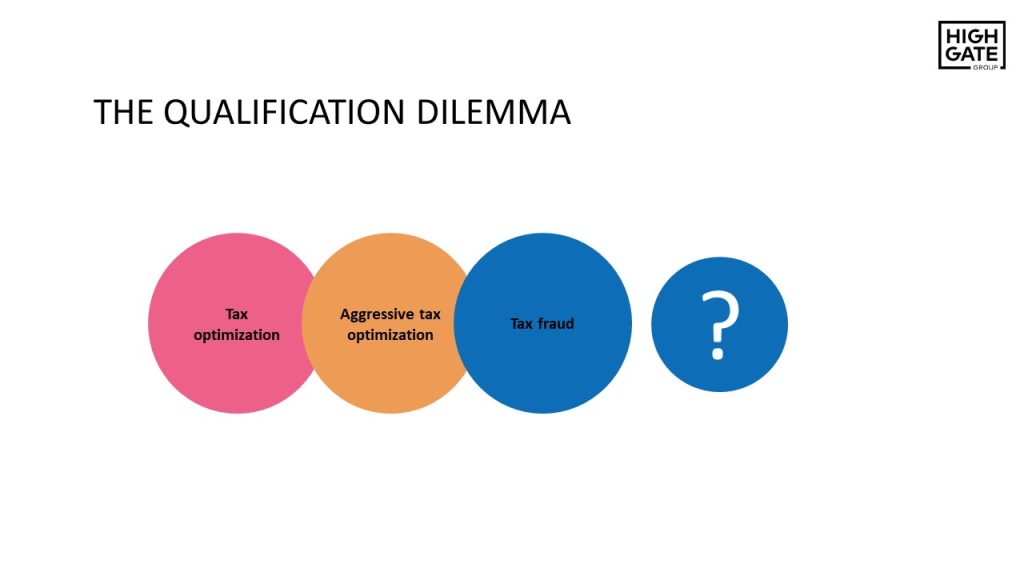

Is setting up and using an offshore company legal?

Slovak measures against offshore companies

Offshore companies & Practical advice

What is an offshore company?

Cryptocurrencies & Offshore company

Is setting up and using an offshore company legal?

Slovak measures against offshore companies

Offshore companies & Practical advice

How much can the Super Deduction save?

Super Deduction & Legal requirements

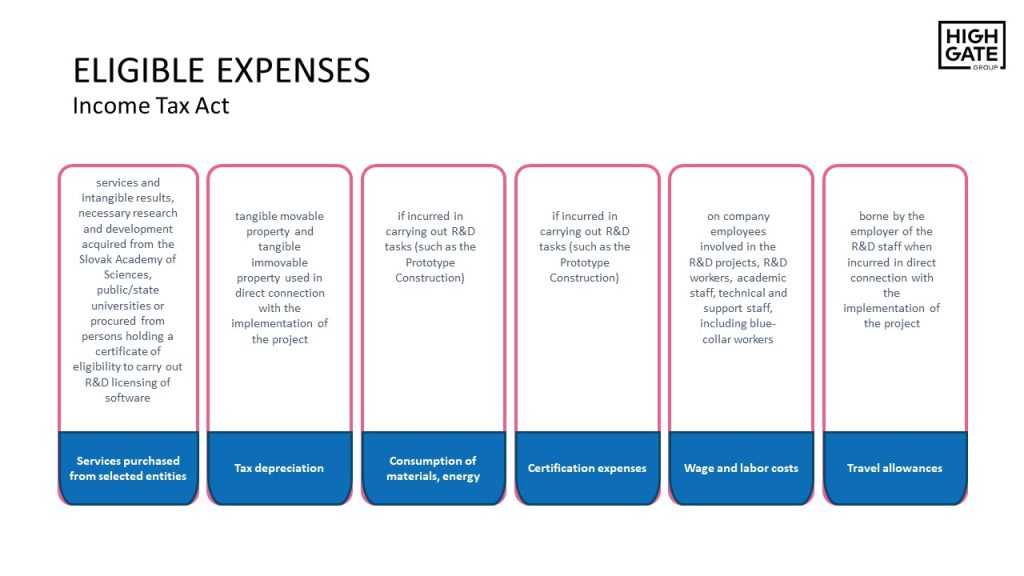

Eligible expenses

Who proves these are R&D activities?

Super Deduction & Tax Audit

Super Deduction - Why work with us?

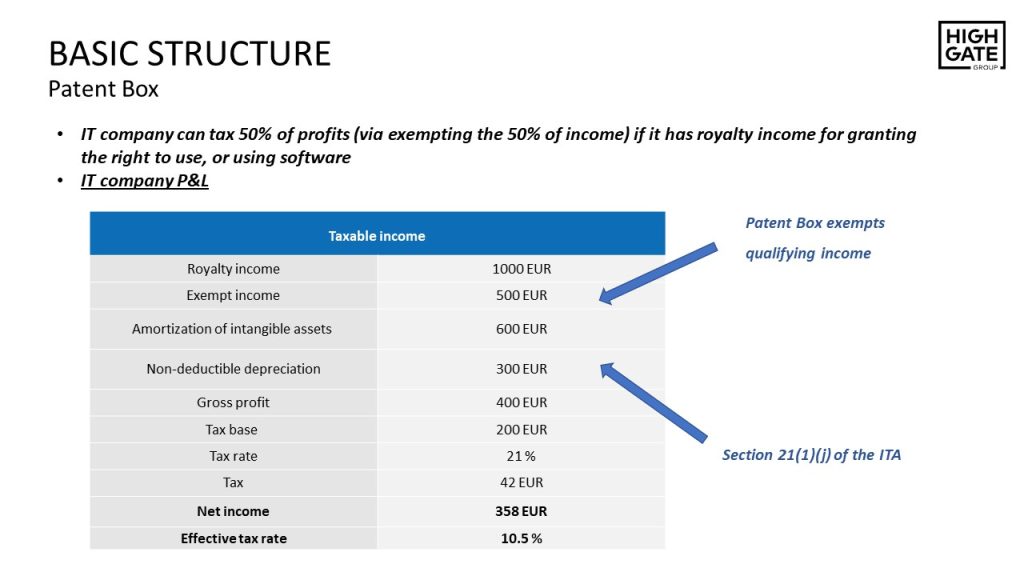

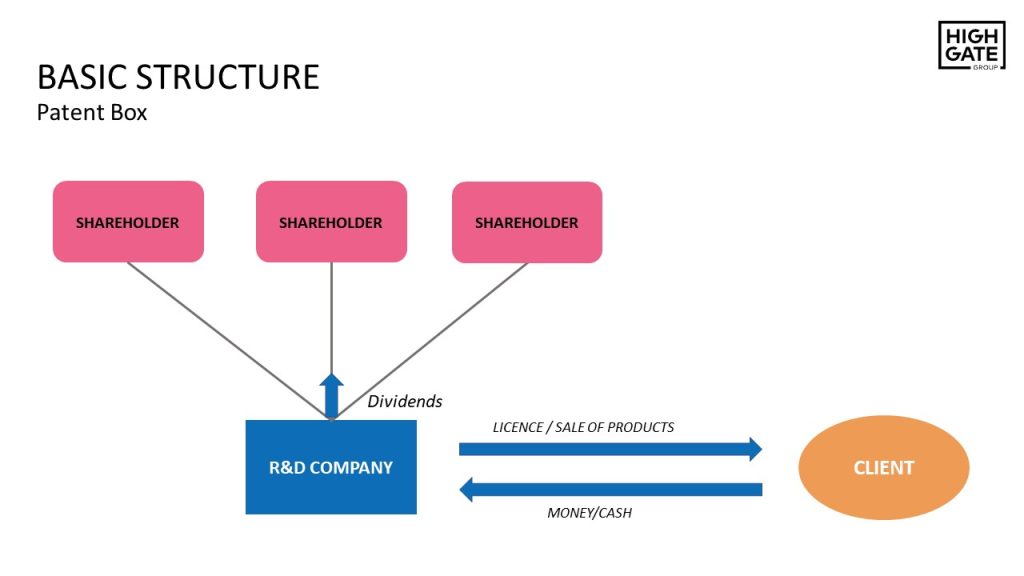

Patent Box in a nutshell

How much can the Patent Box save?

Eligibility for the Patent Box

Does the use of the Patent Box require having employees?

More on the Patent Box

Our Patent Box services

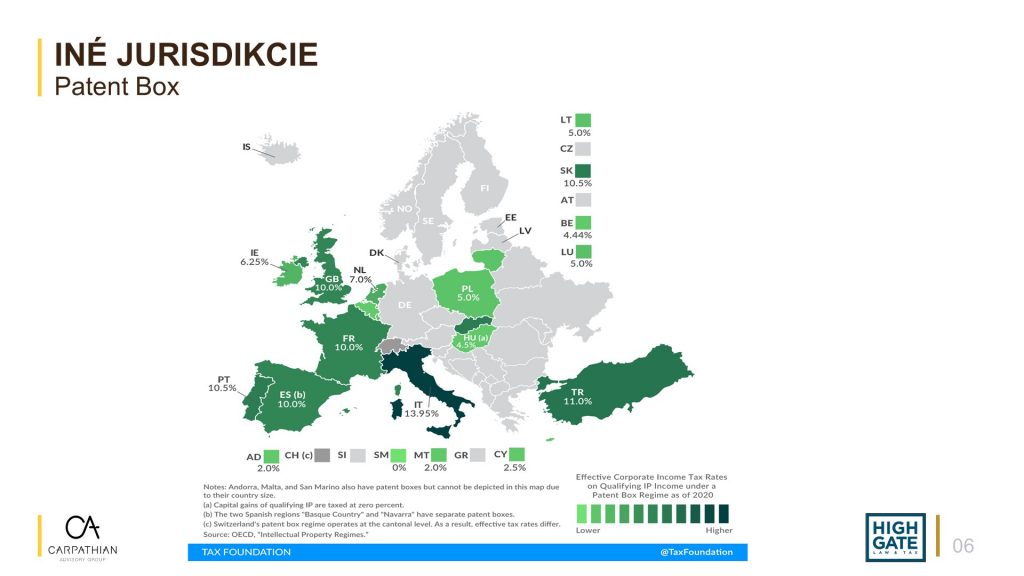

Patent Box history & Patent Box regimes in Europe

Blockchain & Taxes